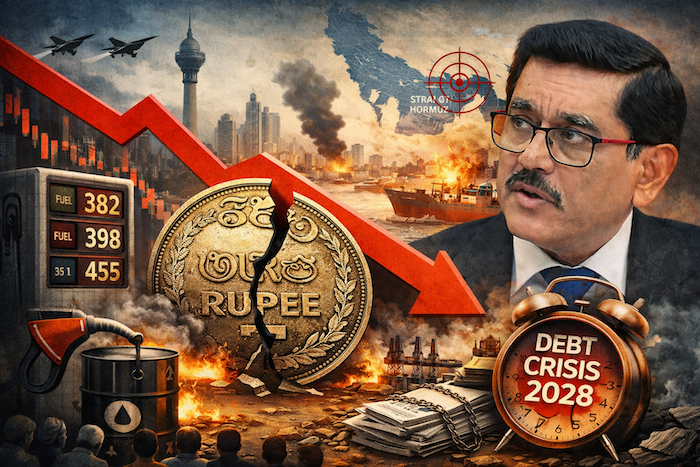

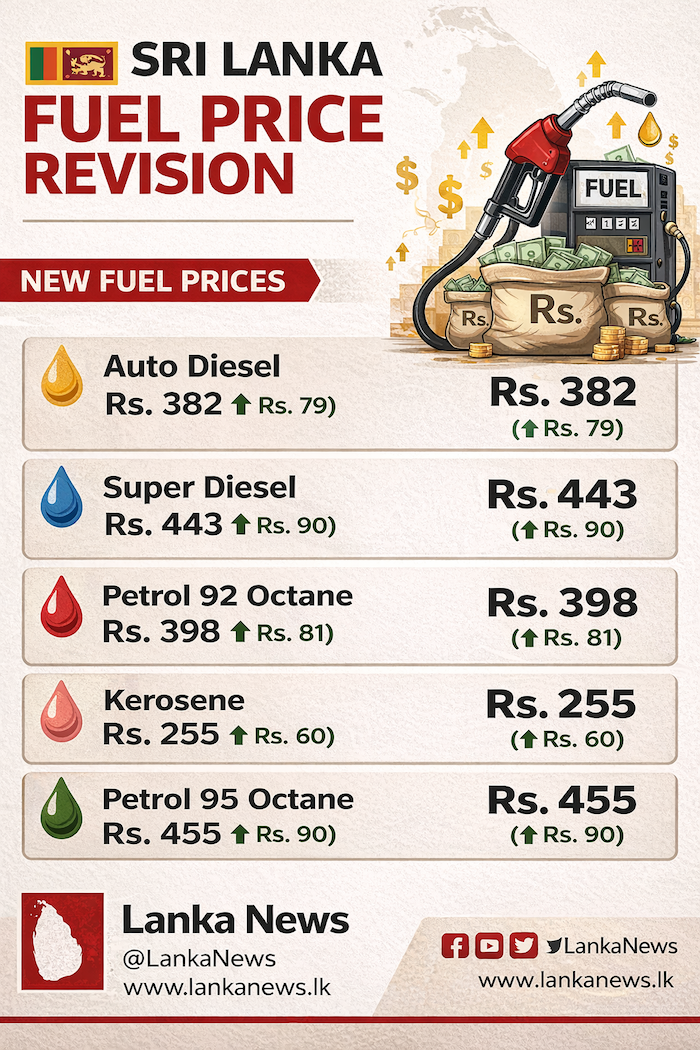

Sri Lanka’s latest fuel price increase has triggered a renewed wave of anxiety across an already fragile economy, raising serious concerns that the country may be edging toward conditions reminiscent of the 2022 economic collapse. The sharp revision by the Ceylon Petroleum Corporation, matched by Lanka IOC, comes at a time when global oil markets are under severe stress while domestic economic resilience remains limited.

The impact is immediate and far-reaching. Fuel costs sit at the core of the entire economic system — influencing transport, logistics, agriculture, fisheries, and manufacturing. Even marginal increases in diesel prices have historically translated into rapid spikes in food and retail prices, and current conditions suggest that a similar pass-through effect is inevitable. Higher fuel import costs are expected to push up transport, electricity, and food prices, placing renewed strain on households whose incomes have yet to recover meaningfully from previous shocks.

This price shock is unfolding against a worsening global backdrop. The ongoing Middle East conflict and disruptions to key oil supply routes have driven global energy prices beyond $100 per barrel, while supply chains remain under pressure. For Sri Lanka, where petroleum imports account for a substantial share of total import expenditure, this exposure is particularly acute. Emerging supply constraints have already led to signs of fuel rationing, pressure on public services, and the need for emergency procurement reviving concerns about scarcity.

At the policy level, the fuel price adjustment is tied to IMF-backed cost-reflective pricing reforms aimed at stabilizing public finances and reducing losses in state-owned enterprises. However, the rigid application of these measures amid escalating global volatility is increasingly being questioned. Critics argue that policy implementation has lacked flexibility and sensitivity to rapidly changing external conditions, amplifying the burden on an already strained population.

Attention has also turned to the leadership of the Central Bank of Sri Lanka and its Governor, Nandalal Weerasinghe. Critics contend that the Central Bank has operated more as a proxy to IMF prescriptions rather than as an independent authority calibrating policy to local realities. They argue that the failure to fully acknowledge emerging risks, combined with overly optimistic public messaging, has undermined confidence. Assurances that the economy has sufficient “space” to absorb shocks now appear increasingly misaligned with the evolving situation on the ground.

“Growth prospects remain positive, and with recovery and reconstruction spending, economic activity could be even stronger in 2026.” – Nandalal Weerasinghe Central Bank Governor

Moreover, the inability to adapt policy direction following significant disruptions including the economic fallout from the Ditwah cyclone, rising global oil prices, and heightened geopolitical tensions has raised concerns about policy judgment. A perceived lack of transparency and reluctance to recalibrate strategies in line with new risks has contributed to a growing credibility gap. In times of economic fragility, trust in institutions depends not only on stability but also on honesty and responsiveness.

More broadly, the current trajectory is beginning to echo elements of the 2022 crisis. Then, as now, Sri Lanka faced a convergence of external shocks, foreign exchange pressures, rising import costs, and declining public confidence. Today, early warning signals are resurfacing fuel queues are beginning to reappear, rationing mechanisms are being reintroduced, and emergency fuel measures are once again under consideration. These developments suggest that underlying structural vulnerabilities remain unresolved.

While macroeconomic indicators such as inflation and foreign reserves may show relative improvement compared to the depths of 2022, deeper structural weaknesses persist. The economy remains heavily import-dependent, exposed to global commodity price fluctuations, and constrained in its ability to cushion citizens from external shocks. Rising energy costs risk triggering not just inflation, but also reduced consumer demand, slowing business activity, and increased social pressure.

The central question now is whether policymakers can respond with sufficient urgency and adaptability to prevent a renewed downward spiral. Without a more flexible and transparent approach one that recognizes the scale of external risks and adjusts both policy and communication accordingly Sri Lanka risks repeating the missteps of the past.

The country is not yet in crisis. But the warning signs are becoming increasingly difficult to ignore.