The Central Bank of Sri Lanka’s recent warning that it is investigating 18 institutions and individuals over alleged illegal plantation-based investment schemes has sparked debate about the broader message being sent to investors and the absence of a clear regulatory framework for alternative investments.

Speaking at a media briefing, Governor Dr. Nandalal Weerasinghe cautioned the public against investing in forest and plantation ventures that promise unusually high returns, describing such offers as unrealistic and potentially fraudulent. While the warning is aimed at protecting investors from scams, critics argue that the statement risks painting all plantation and land-backed investment models with the same brush and exposes deeper regulatory shortcomings.

The issue is further complicated by investor behavior. With banks and finance companies offering relatively low returns to depositors while maintaining high lending rates, many savers have been seeking alternative avenues that promise better yields. Plantation and land-based schemes often appeal to these investors by presenting themselves as “real asset” opportunities rather than financial products

Plantation and agricultural investment models are not inherently illegal and are widely used across the world as legitimate real-asset investment vehicles. Timber funds, agro-investment trusts, and land-backed agricultural ventures operate under regulatory oversight in many countries, offering investors exposure to tangible assets outside traditional banking and financial markets.

In Sri Lanka, however, such ventures fall into a grey area between financial regulation, land transactions, and commercial agriculture. They do not come directly under the supervision of the Central Bank, the Securities and Exchange Commission, or any single regulatory authority when marketed as land ownership, crop-sharing, or lease-based arrangements rather than financial deposits. This regulatory vacuum has allowed some operators to structure schemes in ways that bypass existing financial laws.

Observers note that the Central Bank’s repeated warnings tend to be reactive rather than preventive. By the time investigations are announced, large sums of public funds may already have been mobilized. Without a framework that requires registration, disclosure, and oversight of any entity offering structured returns to the public regardless of whether it is labeled as a deposit, land investment, or agricultural project similar schemes are likely to reappear in different forms.

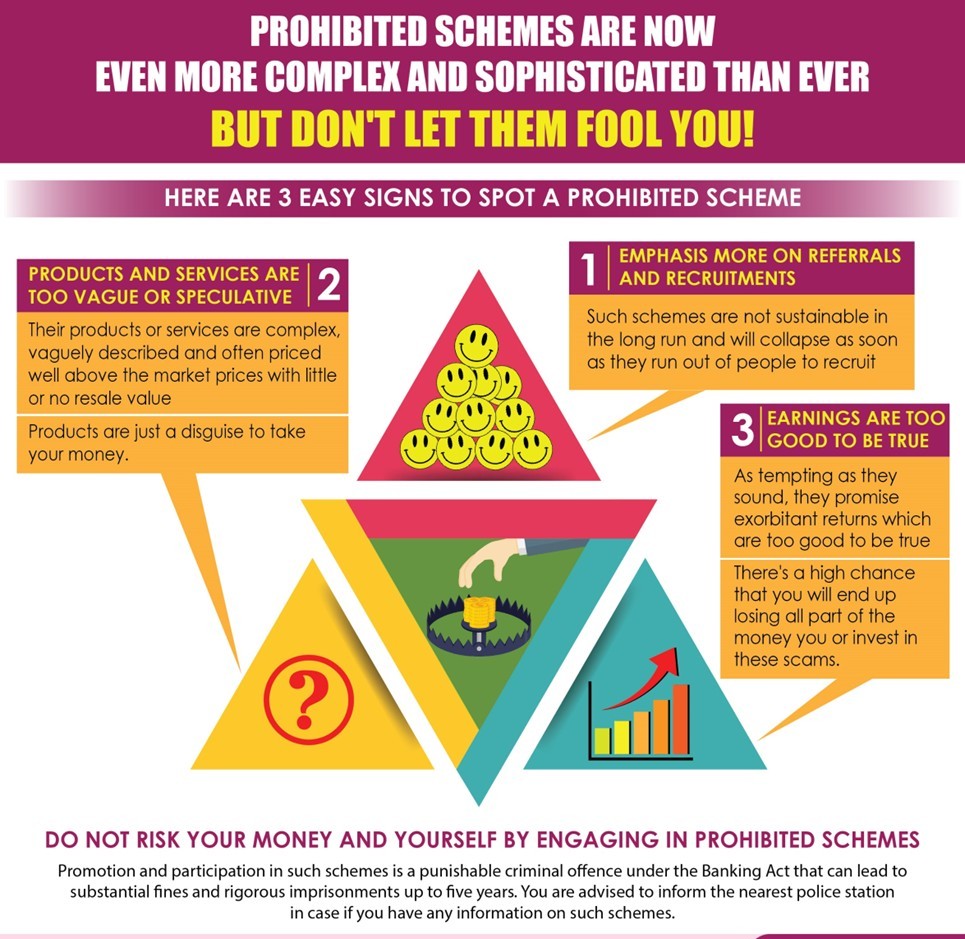

Section 83C of the Banking Act criminalizes any scheme where people are induced to pay money or monetary value and the returns they receive depend mainly on bringing in more participants or on the continued contributions of participants, rather than on genuine economic activity. The law deliberately defines “money” and “monetary value” very broadly so that schemes cannot escape liability by disguising themselves as land sales, crop cultivation projects, eco ventures, or asset-backed investments. Its focus is not on whether land exists, crops are planted, or agreements are signed, but on whether earlier investors are effectively paid from the funds of later investors. This is why many plantation and agricultural “investment” schemes that promise unusually high, regular returns fall within the risk contemplated by Section 83C: when crop cycles cannot realistically generate monthly cash flows, the only source of such payments is typically new investor money. The section also gives the Central Bank wide investigative powers and provides for serious criminal penalties, allowing courts to immediately halt such schemes where a prima facie case exists.

While the Central Bank’s concern about exaggerated return promises such as 30–40 percent per month is widely acknowledged as valid, analysts say the broader solution lies not only in warnings and investigations but in creating a regulatory pathway for legitimate plantation and land-backed investment models to operate transparently.

Calls are now growing for a coordinated framework involving the Central Bank, SEC, and other relevant authorities to bring such alternative investments under structured oversight. Such a move, observers argue, would help distinguish genuine operators from fraudulent ones while giving investors safer options outside conventional banking products.

Until such clarity is introduced, the Central Bank’s warnings, though well-intentioned, may continue to highlight a recurring problem: investment schemes exploiting the spaces between existing laws, and a public left to navigate those spaces with limited protection.