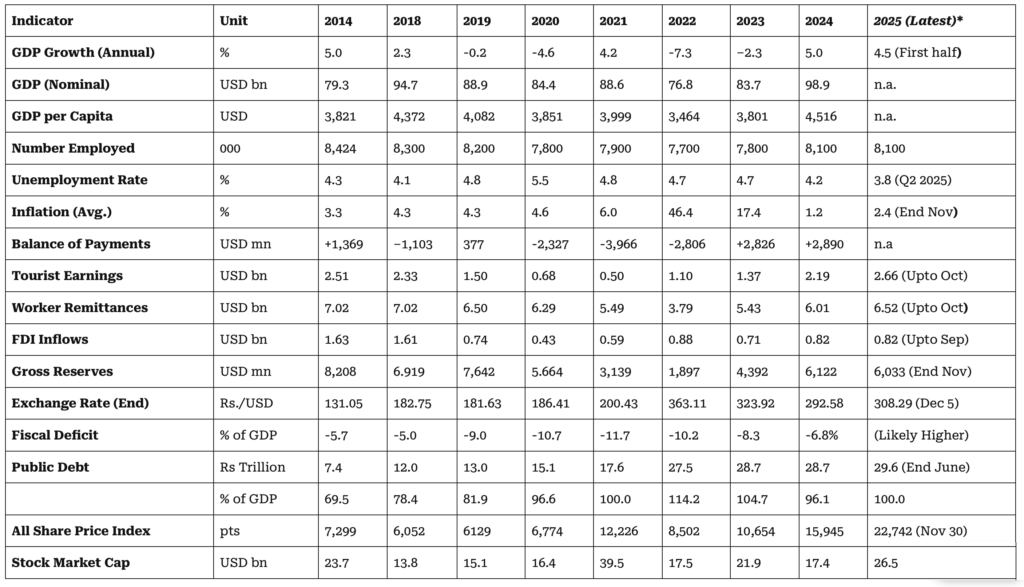

ECONOMIC PERFORMANCE (2018-2024)

What happened to the Economy in 2025?

In 2025, Sri Lanka’s economy had begun to stabilise after years of crisis and contraction, aided by the suspension of external commercial debt repayments, easing inflation, stronger worker remittances, and a rebound in tourism earnings. This fragile recovery, however, has been sharply derailed by Cyclone Ditwah, which struck in late November and caused extensive damage nationwide. The disaster is expected to dampen economic growth, place additional strain on public finances, reignite concerns over debt sustainability, and intensify pressure on households and key sectors such as agriculture, tourism, and infrastructure.

ECONOMIC GROWTH

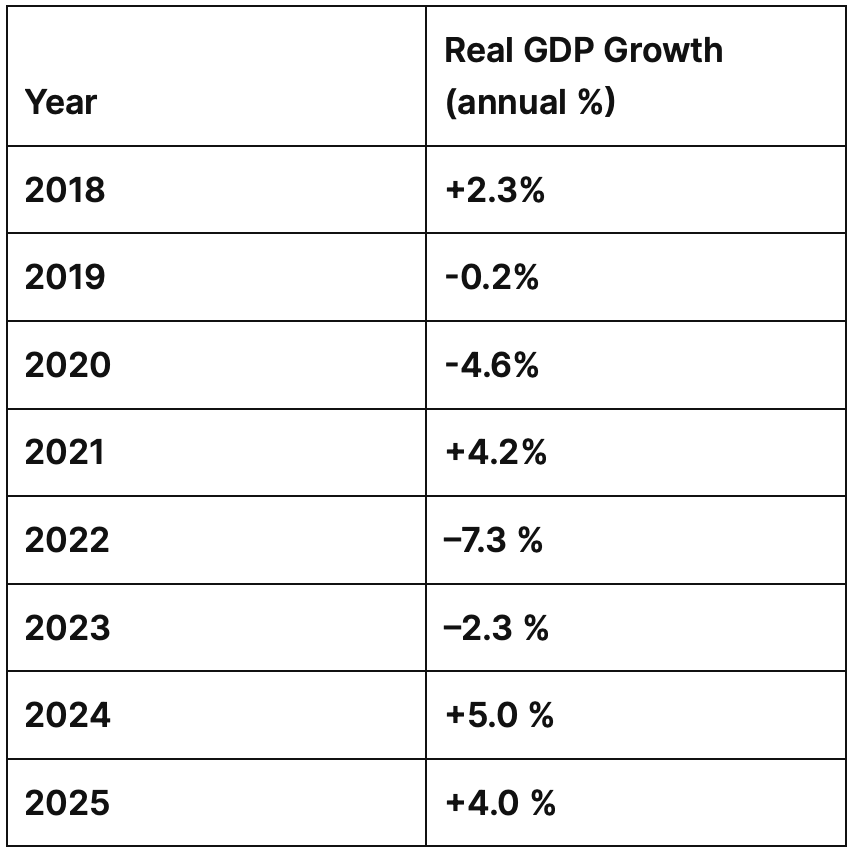

ANNUAL GDP GROWTH RATE

GROSS DOMESTIC PRODUCT (GDP)

GDP PER CAPITA INCOME

A tentative economic recovery took shape in 2025, underpinned by a modest build-up of foreign exchange reserves due to the suspension of loan repayments, easing inflation, stronger remittance inflows, and rising activity across construction, tourism, logistics, ICT, and financial services. While growth remained positive, its momentum was constrained by infrastructure bottlenecks, weak global demand, and persistent fiscal pressures. After years of grappling with low growth, weak investment, and the consequences of macroeconomic missteps, Sri Lanka nonetheless appeared to be drifting back toward a familiar pattern of instability. Despite incremental gains from gradual fiscal consolidation, inflation targeting, and improved foreign inflows, these advances were eroded by short-sighted policy choices, political complacency, and the absence of coherent long-term planning.

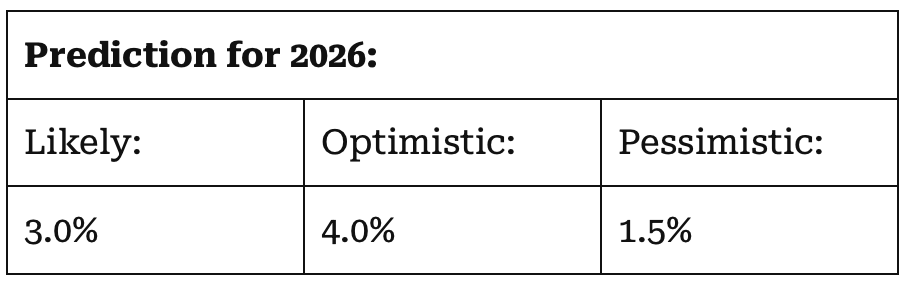

What’s in store in the coming year of 2026?

Sri Lanka’s current macroeconomic fundamentals suggest that the economy has emerged from acute crisis conditions and is moving toward gradual stabilisation. However, growth remains weak from a low base, while inflation has eased from a historically elevated index level. External inflows have improved compared with the contractionary years of the pandemic, yet significant challenges persist in public finances, external debt management, and the recovery of key sectors. Of particular concern is the near absence of new foreign currency debt inflows from bilateral sources.

Looking ahead, sustained fiscal discipline, stronger private-sector investment, and targeted, sector-specific growth strategies could help rebuild business confidence, improve liquidity, ease interest rates, and support a recovery in domestic demand. While these factors could translate into a more meaningful economic upturn in 2026, the government’s current weaknesses in policy execution and implementation cast doubt on the likelihood of such an optimistic outcome.

Outlook for 2026

Sri Lanka’s inflation remained subdued throughout most of 2024–2025, largely reflecting weak domestic demand amid stagnant growth, tight monetary conditions, and a managed exchange rate policy. The low CCPI was driven by a combination of slow economic activity, easing food prices, muted consumer demand, and depressed oil and other essential commodity prices. Despite lower interest rates, demand-side pressures did not materialise, and core inflation stayed well contained.

Looking ahead, inflationary pressures could begin to surface in the second half of 2026 as reconstruction spending and credit growth gradually gather pace, particularly if persistent supply-side constraints are not effectively addressed. These risks are now further compounded by the economic fallout from the escalating Iran–US conflict, which has driven global energy prices sharply higher and disrupted key supply chains. For a fuel-import dependent economy like Sri Lanka, elevated oil prices are likely to raise transportation and production costs across sectors, adding a fresh layer of cost-push inflation.

However, the Central Bank’s inflation-targeting framework, together with the IMF’s continued emphasis on fiscal discipline under its programmes, should serve as a critical anchor against macroeconomic overheating. While cyclone-related disruptions may trigger short-term increases in food prices and construction material costs, and external shocks from the conflict may intensify imported inflation, the underlying inflation trajectory is still expected to remain broadly within the target range, provided policy discipline is maintained and external conditions do not deteriorate further.

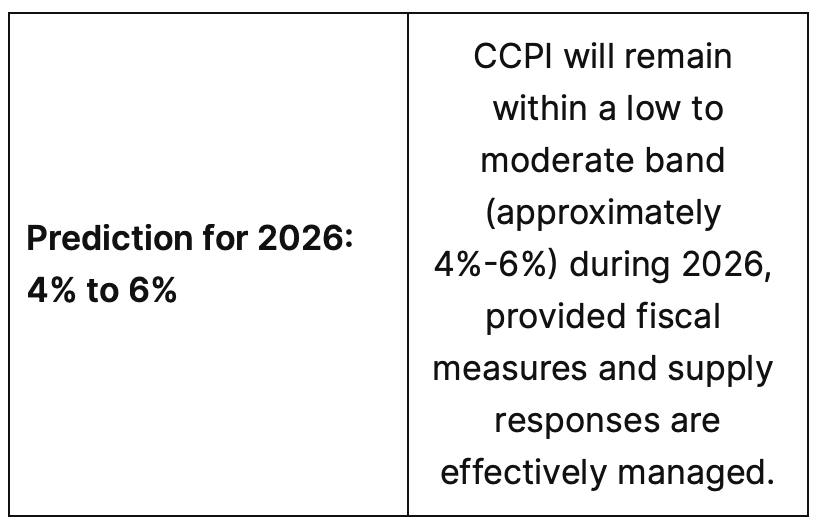

Accordingly, headline inflation is projected to stay in the 4%–6% range in 2026, with only temporary volatility arising from movements in global commodity prices, domestic supply adjustments, and infrastructure-related disruptions.

FOREGIEN EXCHANGE RESERVES

Prediction for 2026

We forecast official reserves to drop to between USD 4.5 – 5.5 billion in 2026,

assuming:

- Continued multi-lateral support

Stable trade financing and remittance flows, plus buoyant Tourism inflows - The Central Bank intervention to supply Forex is curtailed

High duties for vehicle imports continues. - A flexible exchange-rate regime and prudent import management is practiced.

A rise beyond USD 7 billion is possible only if FDI materializes into equity-based flows and reconstruction financing accelerates

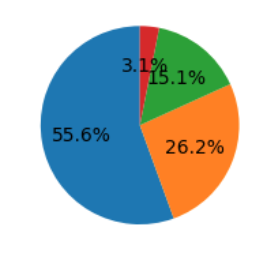

Sri Lanka Reserves Breakdown

Outlook for 2026

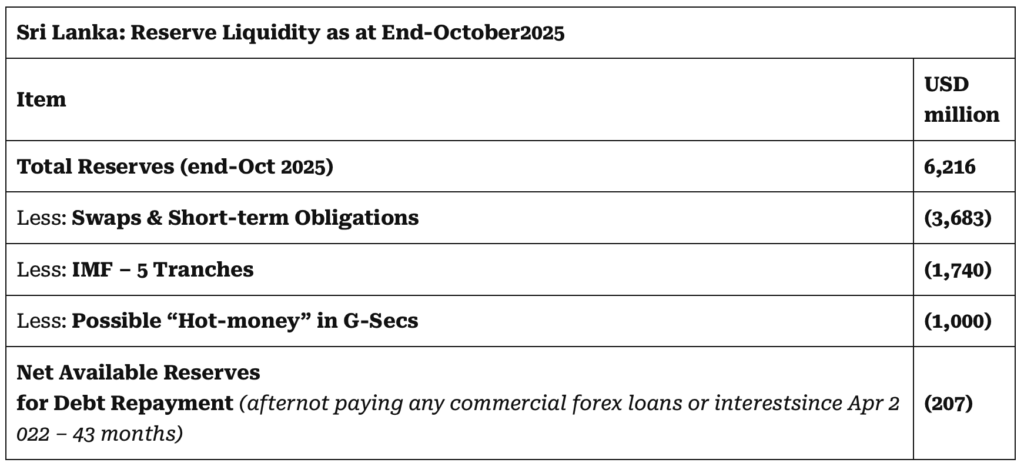

Foreign exchange reserves have strengthened relative to the crisis period, supported by the debt default and higher FX inflows from IMF disbursements, currency swaps, tourism receipts, worker remittances, and short-term “hot money” flows into Treasury bills and bonds. However, underlying or organic reserve accumulation has remained slow, raising serious concerns about Sri Lanka’s capacity to meet foreign currency debt repayments from 2028 onwards, when scheduled obligations resume.

Reserves therefore require prudent management, particularly as import demand is likely to recover gradually and cyclone-related reconstruction activity begins. Sustaining an adequate reserve buffer will depend on maintaining:

- Stable multilateral and bilateral financial support.

- Steady growth in remittances through formal channels,

- Strong performance in service exports such as ICT, tourism, and logistics,

- Timely implementation of energy sector investments, and

Sri Lanka’s foreign exchange reserves are likely to face renewed pressure in 2026, even as near-term debt-service obligations remain contained following the external default, tourism earnings continue to recover, and multilateral financing flows persist. The escalation of the US–Iran conflict has added a significant external headwind, driving up global energy prices and increasing the country’s import bill, thereby accelerating foreign currency outflows. As a fuel-import dependent economy, Sri Lanka is particularly exposed to these shocks, which heighten the risk of reserve erosion.

At present, reserve accumulation remains heavily reliant on short-term borrowings and IMF-related inflows rather than on structurally strong and sustainable sources. The US–Iran war has further complicated this dynamic by disrupting global capital flows and reinforcing a risk-averse investment climate. This reduces the likelihood of meaningful inflows through foreign direct investment and portfolio channels, limiting Sri Lanka’s ability to organically rebuild reserves.

In addition, heightened geopolitical tensions have contributed to increased volatility in global financial markets and shipping costs, placing further strain on the external account. While tourism and remittances may provide some buffer, their resilience could be tested if the conflict dampens global growth or travel sentiment.

Addressing these vulnerabilities will require timely and credible policy responses aimed at strengthening durable sources of foreign exchange. This includes improving the investment climate to attract stable FDI, enhancing export competitiveness, and maintaining macroeconomic stability to sustain investor confidence. In an environment shaped by the US–Iran conflict and elevated external uncertainty, building a more resilient reserve position will be critical to safeguarding Sri Lanka’s external stability.

INTEREST RATES

BENCHMARK INTEREST RATE

PRIME LENDING RATE

| Prediction for 2026: | |

| Likely to Rise | As borrowing demand rises andgrowth falters, interest rates may gradually rise, but are unlikely to return to previous crisis-level highs unlessthere is some political turmoil. |

Outlook for 2026

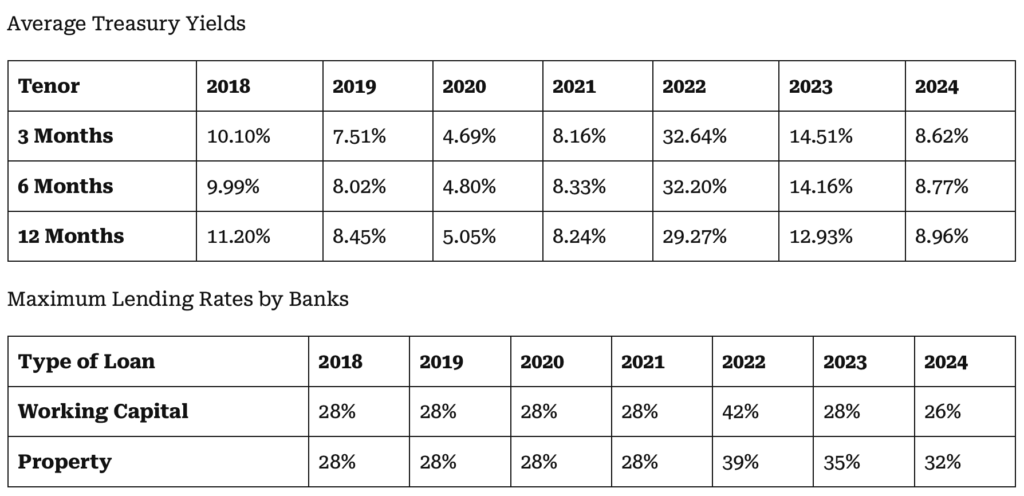

Interest rates in Sri Lanka increasingly reflect the constraints of the IMF-supported adjustment programme, with Treasury yields remaining elevated relative to prevailing inflation. This dynamic has been reinforced not eased by the escalation of the US–Iran conflict, which has tightened global financial conditions and heightened risk aversion across emerging and frontier markets. As global investors retreat to safe-haven assets amid geopolitical uncertainty, domestic yields have remained sticky, limiting the Central Bank of Sri Lanka’s (CBSL) room to calibrate a more growth-supportive monetary stance.

While political stability and continued adherence to the IMF framework have strengthened macroeconomic discipline, they have also narrowed policy flexibility at a time when external shocks are intensifying. The persistence of interest rates at levels arguably higher than warranted has diluted the potential gains from fiscal consolidation. In particular, elevated borrowing costs—now compounded by war-driven global volatility have constrained public investment, undermining efforts to stimulate growth through capital expenditure.

Despite IMF oversight, lending rates have not eased meaningfully, continuing to weigh on businesses and households. The spillover effects of the US–Iran war especially through higher energy costs, imported inflation risks, and tighter global liquidity have further complicated the interest-rate outlook. Financial conditions remain restrictive, discouraging private-sector borrowing and delaying investment decisions.

Although stress within the banking sector has moderated and non-performing loans have stabilised, this has largely been due to subdued credit growth rather than a broad-based improvement in borrower strength. Underlying vulnerabilities persist, particularly in sectors such as agriculture, tourism, and small and medium-sized enterprises, which are highly sensitive to both domestic cost pressures and external demand shocks linked to the conflict.

In this environment, establishing a more predictable and moderately priced interest-rate structure is critical for restoring financial-sector confidence and enabling capital formation. However, this will depend not only on domestic policy credibility but also on the trajectory of global conditions shaped by the US–Iran war. Meanwhile, modest foreign participation in government securities has helped contain excessive upward pressure on yields and limit currency volatility, though these inflows remain vulnerable to sudden reversals if geopolitical risks intensify further.

Against this backdrop, market interest rates are expected to edge higher in 2026, although there may be room for moderate easing if domestic liquidity improves through stronger foreign exchange inflows linked to cyclone relief and reconstruction support. While short-term borrowing needs are likely to rise to fund rebuilding and infrastructure requirements, the policy discipline imposed under the IMF programme should help contain excessive interest-rate volatility, despite ongoing inefficiencies in government execution.

GOVERNMENT DEBT

| Prediction for 2026: | |

| Projected Debt (end 2026) Rs.32 Trillion | Government debt is expected to increaserapidly in nominalterms, and the pace may even increase duringthe 2026, unlessrevenue growth is maintained. |

Outlook for 2026

Borrowing pressures and associated risks remained elevated in 2025, with the overall risk profile continuing to widen, even as domestic markets absorbed issuances at lower yields for a limited period.

Looking ahead to 2026, the greater risk is not excessive borrowing but underinvestment and an inability to generate sufficient economic growth, which would ultimately undermine debt-servicing capacity over time. Sri Lanka’s financing needs are therefore expected to remain substantial, driven by high interest costs, challenging rollover requirements, post-disaster reconstruction spending, and funding demands from state-owned enterprises. While debt restructuring agreements have temporarily eased immediate repayment pressures, they effectively represent a deferral rather than a resolution, implying that sustained borrowing will still be required to manage maturing domestic obligations, maintain essential public services, and finance critical infrastructure.

However, future debt sustainability cannot be a reality unless:

- There is an immediate healthy GDP growth and export diversification which would reduce reliance on external debt

- Borrowing supports productive investment, not recurrent spending

- Interest costs are reduced substantially.

- Reconstruction and infrastructure spending is executed efficiently and transparently

The main challenge for the Government therefore would be to enhance the quality and purpose of debt, especially borrowing used to fund growth- enhancing capital investment.

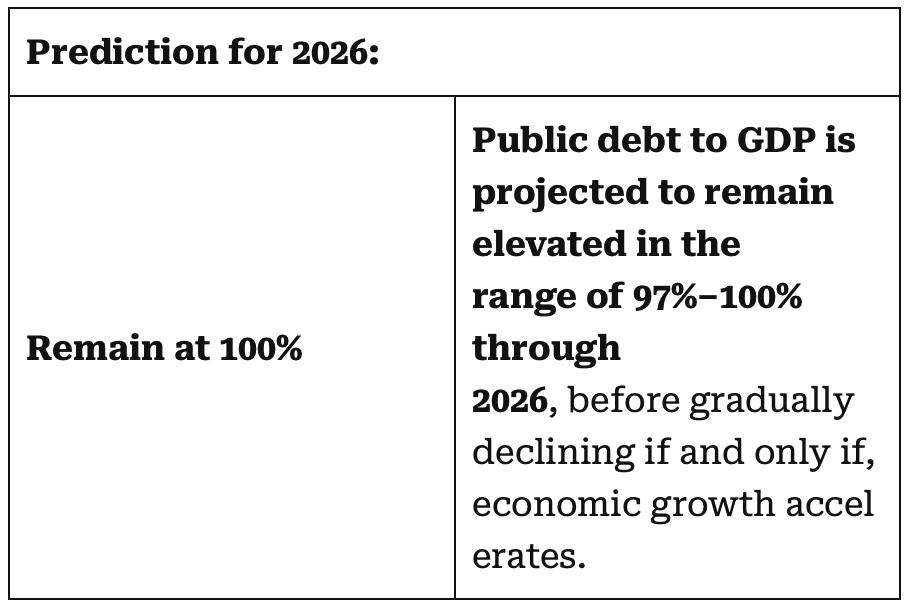

DEBT TO GDP

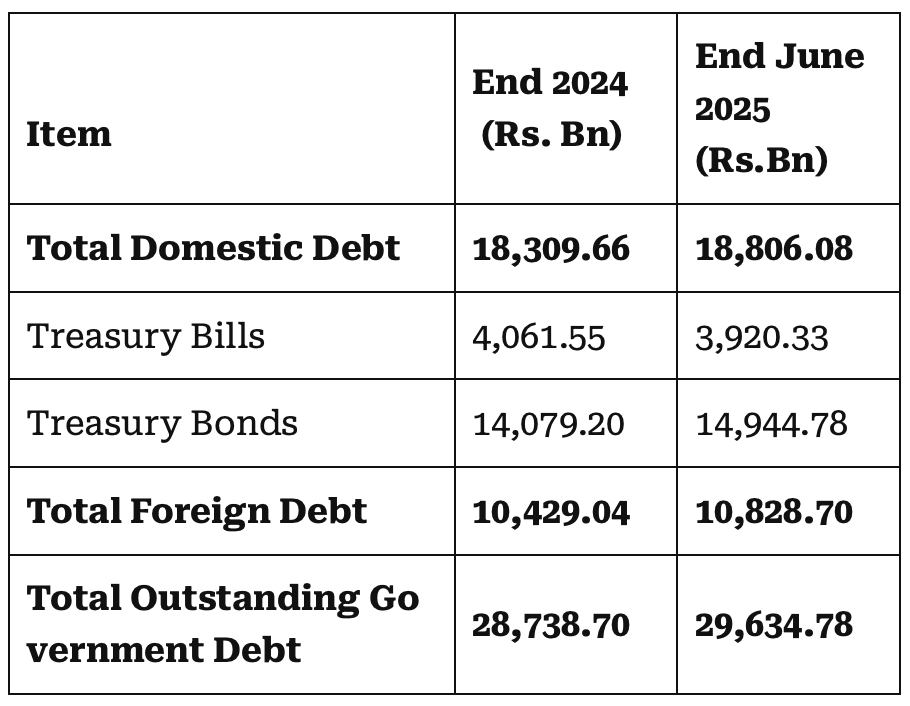

Outstanding Public Debt as at end June 2025

Outlook for2026

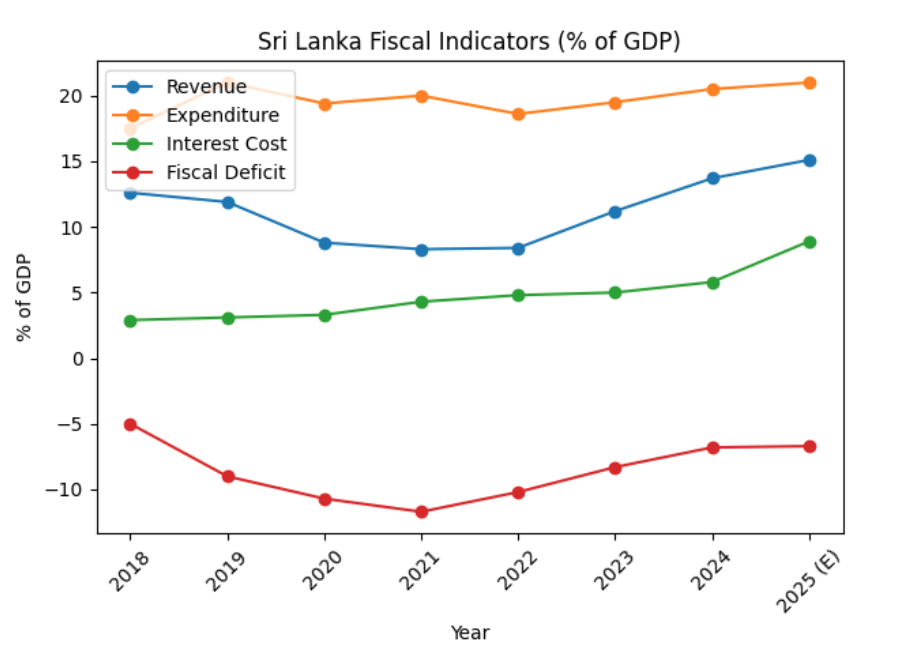

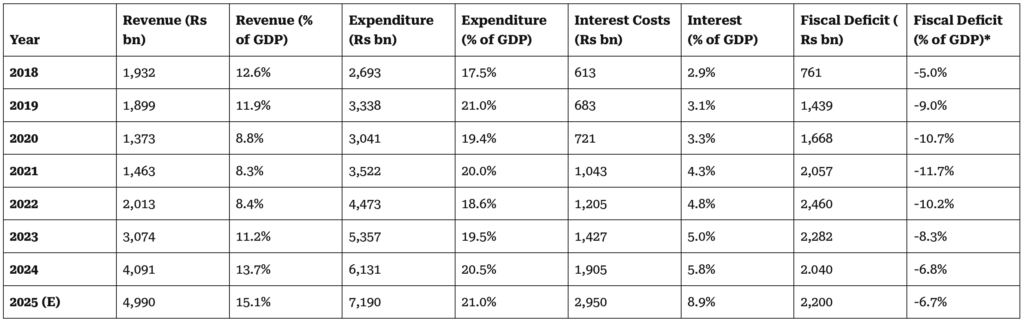

Sri Lanka’s debt burden remained exceptionally high in 2025, even after the completion of both domestic and external debt restructuring. Gains in revenue mobilisation—achieved partly at the expense of economic growth—together with tight expenditure controls and policy continuity under the IMF programme, have helped stabilise the overall debt position. Nonetheless, social protection spending continues to exert fiscal pressure, although historically loss-making state-owned enterprises (SOEs) have begun to return to profitability following the implementation of IMF-backed cost-recovery mechanisms.

The public debt-to-GDP ratio remained broadly stable in 2025 after several years of sharp increases from its 2014 low of around 69%. While debt default and restructuring have reduced near-term repayment risks, and stronger revenue performance has delayed immediate stress, elevated interest costs continue to pose a significant medium-term risk to debt sustainability.

Over the next two years, sustained progress in this ratio will depend on:

- Achieving and sustaining strong economic growth

- Reducing dependence on transfers and subsidies to state-owned enterprises

- Improving the efficiency of government capital expenditure, particularly in infrastructure development

- Ensuring consistent tax administration and broadening the tax base

- Reversing policies that have dampened economic growth

- Avoiding ad hoc and unplanned public spending

A meaningful improvement in the debt ratio beyond 2026 will depend on real GDP growth being consistently above 5.0%, improved export earnings, a strengthening LKR, continued fiscal discipline, and productive investment that supports long-term capacity building. As to whether there would be credible plan ensure such outcomes remains to be seen.

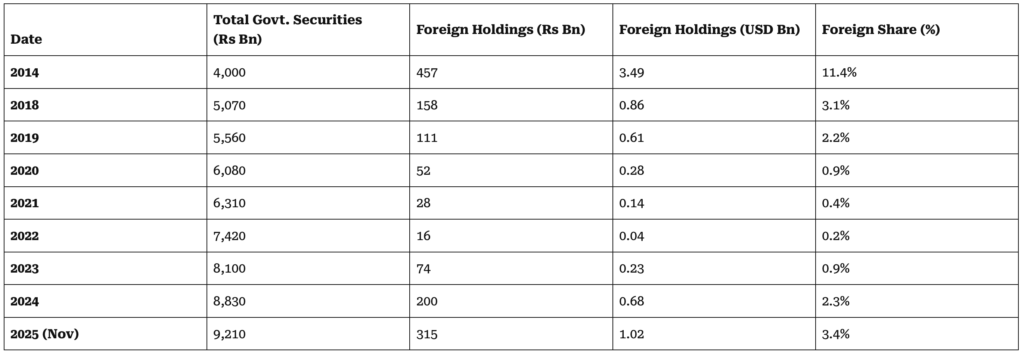

FOREIGN HOLDINGS IN GOVERNMENT SECURITIES

Prediction for 2026:

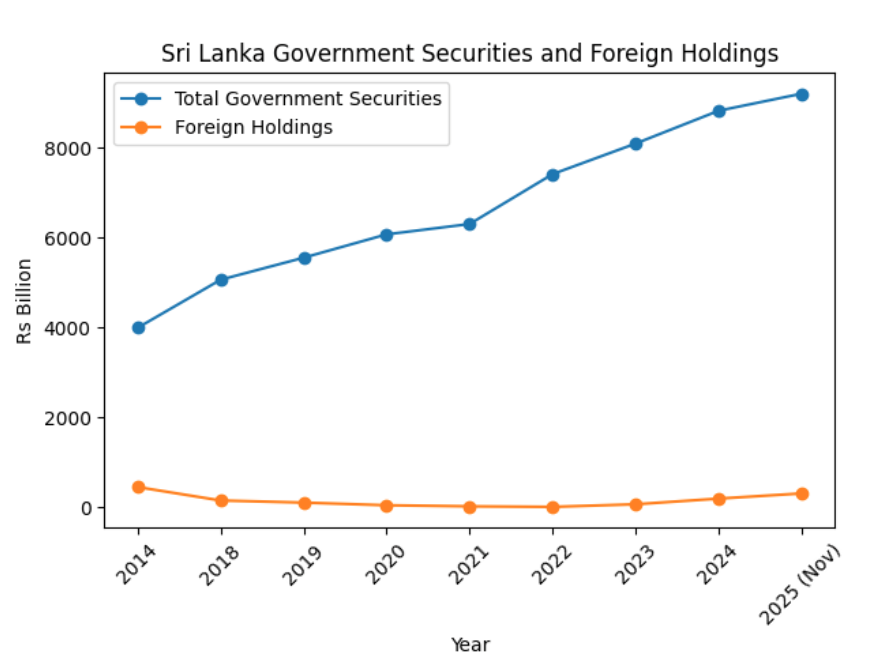

Foreign holdings will remain in the range of 1%–1.5% of outstanding government securities in 2026, but exit fast, if debt vulnerabilities escalate.

Outlook for 2026

Foreign investor participation in Sri Lanka’s government securities has started to recover after plunging to historic lows during the 2020–2022 crisis. Lower near-term repayment risks, subdued inflation, and expectations of exchange rate and interest rate volatility appear to have attracted foreign “hot-money” investors seeking exposure to frontier-market debt.

Although short-term movements in global interest rates may influence the direction and scale of these flows, the prevailing trend reflects opportunistic, short-duration positioning aimed at capturing near-term gains. This has helped compress Treasury bill and bond yields in the short run, offering some temporary relief to domestic financing conditions.

Going forward, the sustainability of foreign inflows will hinge on global rate dynamics, IMF-related developments, exchange rate stability, and overall market liquidity. Should inflation remain well contained and the external sector continue to recover, a gradual increase in foreign holdings of government securities is likely.

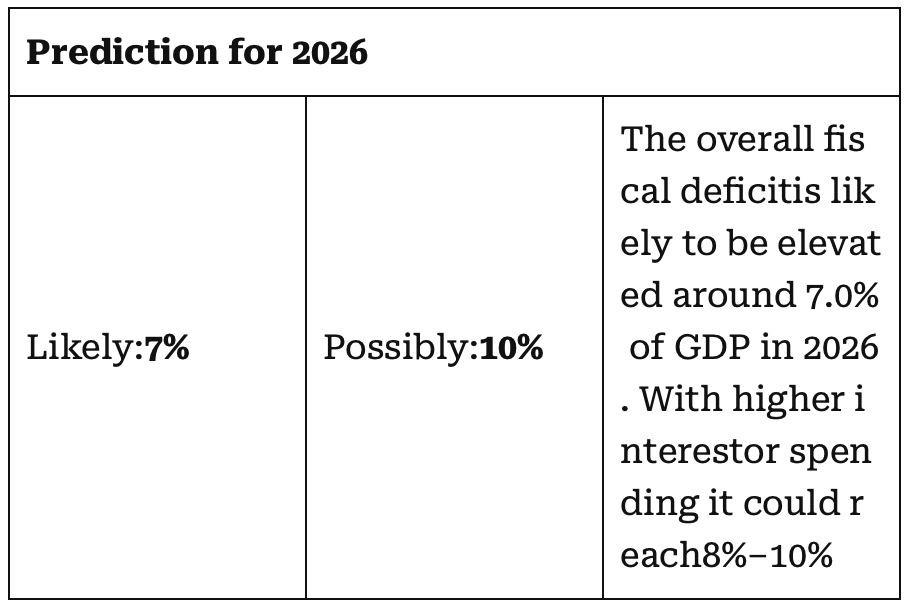

FISCAL DEFICIT

Outlook for 2026:

Government revenue collection has improved on the back of tax administration reforms, tighter exemptions, stronger compliance mechanisms, and adjustments to the tax structure. However, these gains are increasingly being tested by the economic spillovers from the escalating Iran–US conflict, which has pushed global energy prices higher and raised import costs. This, in turn, could dampen domestic economic activity, weigh on consumption, and create challenges for sustaining revenue momentum, particularly in fuel-sensitive sectors.

At the same time, overall expenditure pressures remain elevated due to exceptionally high interest costs, ongoing social support programmes, infrastructure demands, and post-disaster reconstruction spending following recent weather-related disruptions. The surge in global oil prices linked to the conflict is also expected to increase the Government’s fuel subsidy burden and operating costs, further straining public finances. As a result, the fiscal deficit is likely to remain elevated in 2025, with downside risks emerging if external shocks persist or intensify.

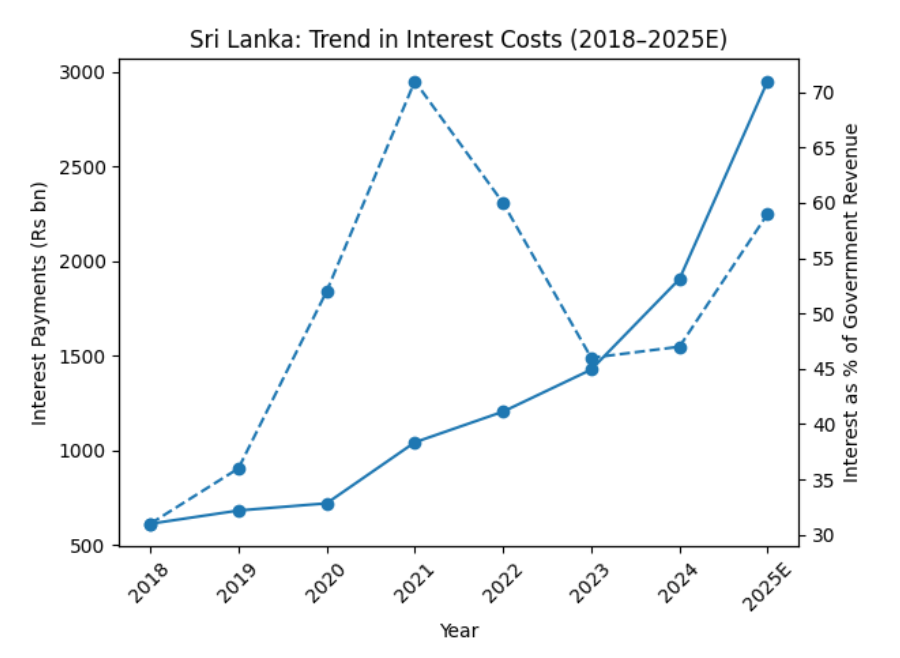

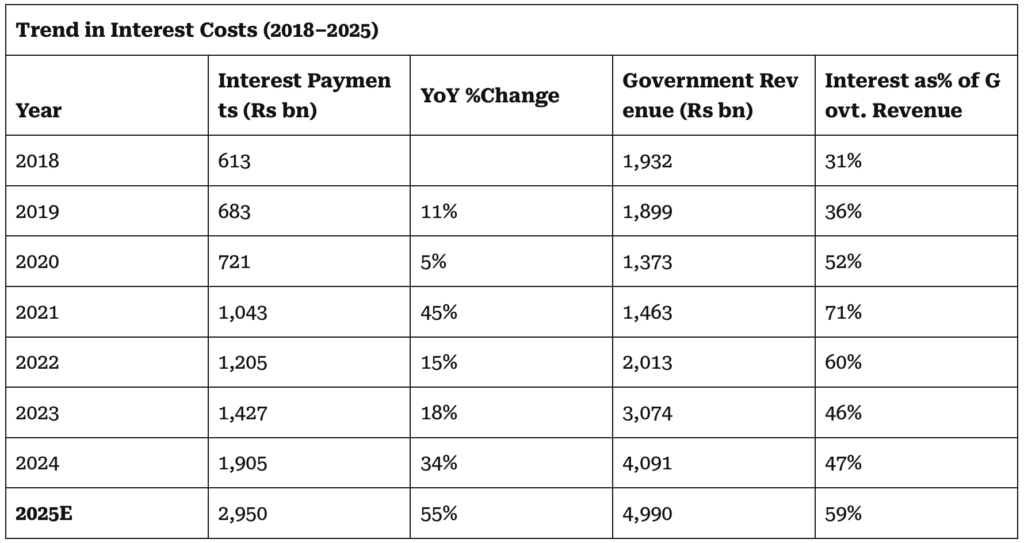

While fiscal data for 2024–2025 show a clear improvement in revenue performance, a key concern is that the bulk of these gains has been absorbed by rapidly rising interest costs, leaving fiscal deficits stubbornly large. In 2022, government interest payments amounted to Rs. 1,205 billion, or 4.8% of GDP, against revenues of Rs. 2,132 billion, or 8.4% of GDP. IMF-driven revenue enhancement measures took effect from 2023 onwards; however, by 2025, interest costs are projected to surge to around Rs. 2,950 billion, while revenues are estimated to increase to Rs. 4,990 billion. This implies that roughly Rs. 1,745 billion of additional interest expenditure—relative to 2022 levels—will be incurred in 2025, largely reflecting the high interest rate environment maintained under IMF-guided monetary policy. This stance has also contributed to widespread financial distress among businesses and households between 2022 and 2025, as many struggled to service elevated borrowing costs.

Looking ahead, the fiscal deficit is expected to widen further in 2026, driven by persistently high interest expenses, reconstruction-related outlays, and sector-specific support measures. These pressures are likely to be exacerbated by the economic fallout from the escalating Iran–US conflict, which has elevated global energy prices and increased the cost of imports, particularly fuel. For Sri Lanka, this not only raises direct fiscal burdens through higher energy-related expenditures and potential subsidies but also indirectly strains public finances by dampening economic activity and weakening revenue performance.

There is therefore a material risk that the fiscal consolidation trajectory could be undermined, even if capital spending remains well targeted and tax exemptions are tightly controlled. Reconstruction following recent climate-related shocks, rising social protection needs, and higher growth-supportive capital expenditure will add to short-term deficit pressures, while any slowdown in economic activity—potentially intensified by external shocks from the conflict—could further weaken tax revenues in 2026. Fiscal space is likely to remain constrained until growth gains firm traction, external conditions stabilise, and the full benefits of debt restructuring are realised.

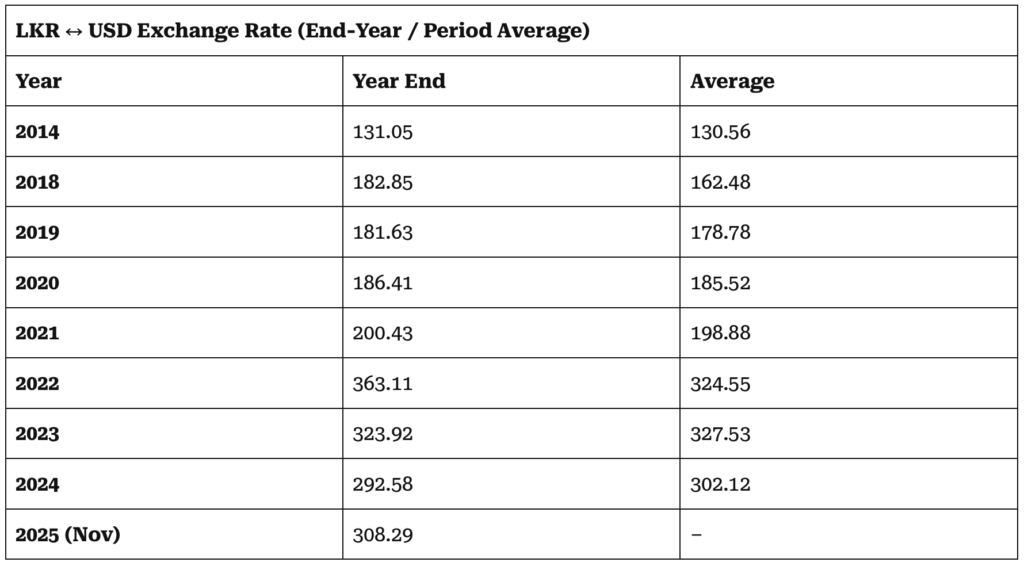

EXCHANGE RATE

Prediction for 2026:

LKR is likely to depreciate to around Rs.325-350

per USD range during 2026, notwithstanding intervention by the Central Bank.

Outlook for 2026

The LKR has has been reasonably stable compared to its value at the start of the IMF programme. This is probably due to:

- Non payment of Forex commercial debt for 43 months, so far

- Strong inflows from tourism and remittances

- Large quantum of SWAPs

- IMF funds flow into the Reserves

- “Hot-money” inflows into T/Bills and Bonds

- Lower domestic demand limiting non-essential imports due to slow growth of the economy.

Despite stabilization, the LKR is unlikely to remain flat in the near term. The IMF-monitored “flexible” exchange rate seems to have been artificially controlled to prevent from depreciation in 2025.

Over the next year-2026, the maintenance of the LKR value will depend primarily on:

- Strength of service exports (ICT, tourism, worker remittance, logistics)

- FDI materialization in energy, infrastructure, and real estate.

- Domestic inflation, relative to global trends

- Investor Confidence

- Entry and exit of “hot-money” investments in G-Secs

- Perception about debt repayment ability in 2028

Overall, temporary pressures may also arise from reconstruction-related imports, exchange-rate flexibility and foreign inflows related to multi- lateral financing, PPP projects, and energy investments.

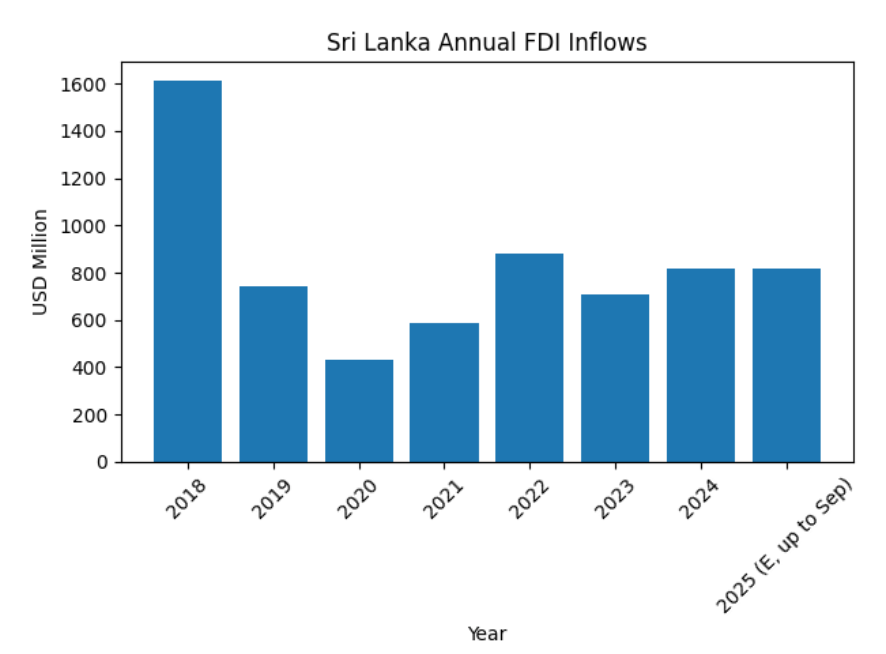

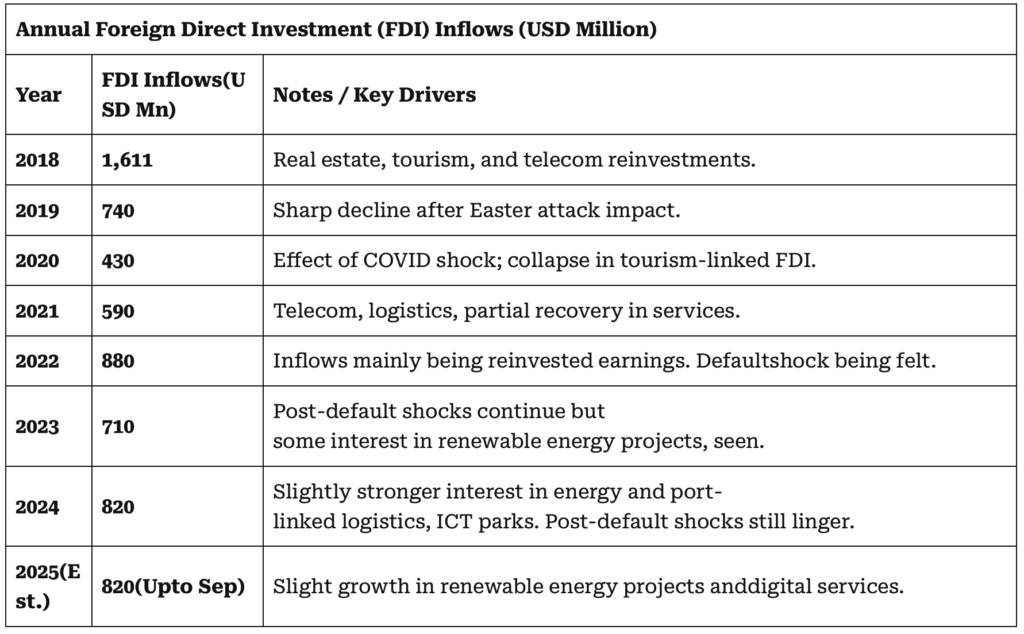

FOREIGN DIRECT INVESTMENTS

Prediction for 2026:

Likely to be

less than USD 1.0 billion,

(<1% of GDP)

Outlook for 2026

FDI inflows in 2025 were expected to recover from crisis-era lows, driven by investor interest in infrastructure partnerships, renewable energy, technology services, and niche export-oriented manufacturing. However, actual inflows fell well short of potential, constrained by institutional delays, regulatory bottlenecks, and elevated global financing costs. These shortfalls have been further accentuated by the escalating Iran–US conflict, which has intensified global uncertainty, disrupted capital flows, and reinforced a cautious, risk-averse stance among international investors toward emerging and frontier markets.

Higher energy prices and increased volatility in global financial markets have also eroded investor confidence, particularly for long-term, capital-intensive projects in smaller economies. Whether this latent investor interest ultimately converts into durable long-term capital will therefore depend not only on sustained policy consistency, regulatory clarity, and faster execution of approved projects, but also on an improvement in global risk sentiment. In this environment, Sri Lanka’s ability to maintain macroeconomic stability and present a credible, reform-driven investment narrative will be critical in mitigating the adverse spillovers from ongoing geopolitical tensions.

Sri Lanka’s current FDI outlook remains subdued, as investor-unfriendly policies, the lingering stigma of debt default, and concerns over macroeconomic stability continue to weigh on sentiment. While global uncertainty and elevated interest rates are likely to further dampen large-scale greenfield investments, selective strategic inflows may still materialise in areas such as renewable energy, logistics, ICT services, real estate–linked developments, and infrastructure partnerships.

Nevertheless, it is now time for Sri Lanka to prioritize quality FDI, with a focus on:

- Export value addition

- Up-market real estate

- Technology transfer and skilled employment

- Domestic supply-chain integration

- Partnerships in renewable energy, logistics, and digital trade

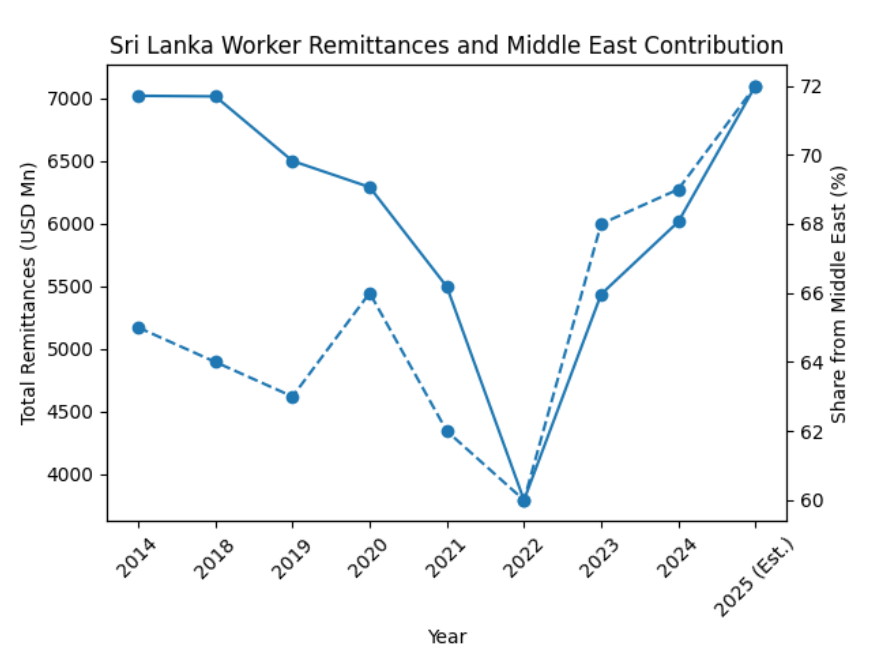

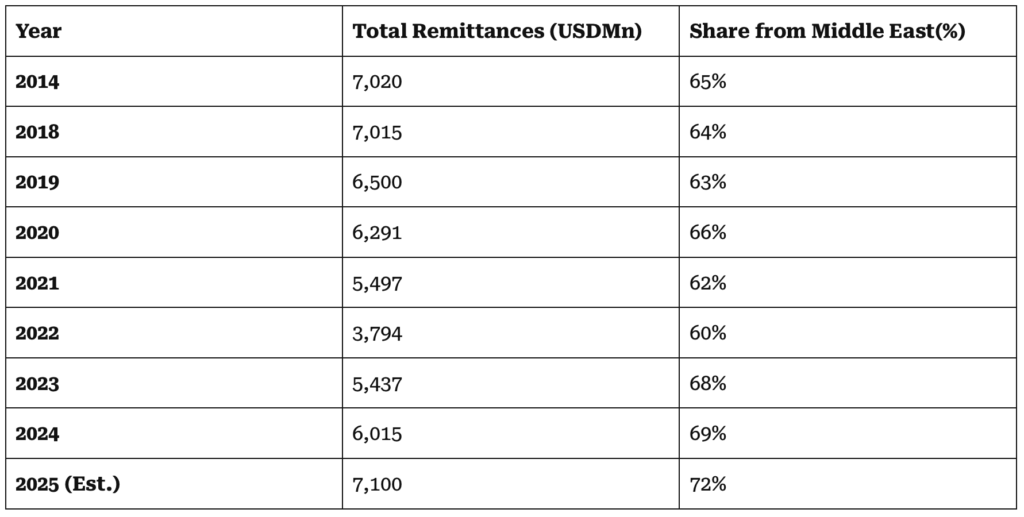

FOREIGN REMITTANCES

Prediction for 2026:

Worker remittances in 2026 to be in the range of USD 7.3 – 7.5 bn with around 70% estimated to originate from the Middle East

Outlook for 2026

Worker remittances maintained stable double-digit growth in both 2024 and 2025, providing crucial support to Sri Lanka’s external sector during the recovery phase. A partial easing of global inflation and strengthening labour markets in the Gulf helped sustain overseas worker incomes, while higher deployment of Sri Lankan workers to construction and service sectors across GCC countries further boosted inflows in 2025.

However, this positive trend faces emerging downside risks from the escalating Iran–US conflict. Given that a substantial (70%) share of Sri Lanka’s remittances originates from the Middle East, any disruption to economic activity in the Gulf region could have a direct impact on inflows. Heightened geopolitical tensions may lead to slower growth in key sectors such as construction and services, where many Sri Lankan workers are employed, potentially affecting job security, wages, and remittance capacity.

In 2026 too, worker remittances are expected to remain strong and continue as the single largest source of foreign exchange for Sri Lanka.

Higher wages in GCC economies, improved foreign employment placements, and incentives to use formal remittance channels are supporting continued inflows. While oil price volatility could influence remittance growth at the margin, labour demand in construction, logistics, healthcare, and domestic services across Saudi Arabia, the UAE, Qatar, and Kuwait is expected to remain strong. The expansion of digital remittance platforms and banking incentives is also helping reduce leakages to informal channels. Nevertheless, a sharp acceleration in remittance inflows appears unlikely in 2026, with growth expected to remain gradual rather than dramatic.

BALANCE OF TRADE

EXPORTS

IMPORTS

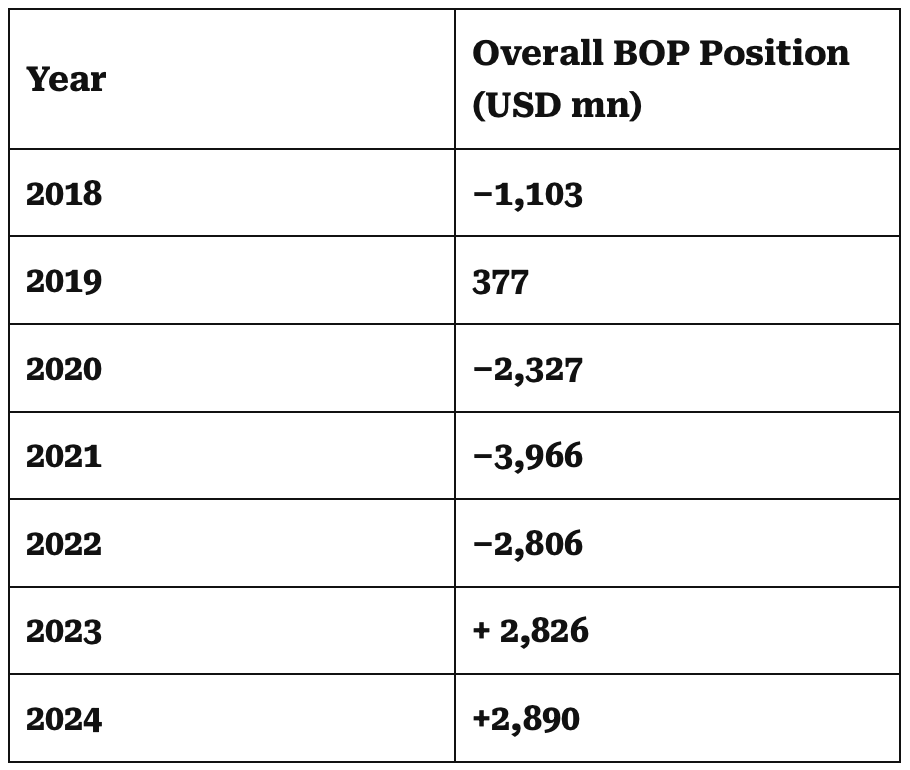

BALANCE OF PAYMENT

Balance of Payments

Prediction for 2026: Moderately Positive

Outlook for 2026

Sri Lanka’s balance of payments (BOP) has proven considerably more resilient than during previous crisis episodes, supported by the recovery in tourism, growth in ICT exports, improved worker remittances following the Covid-19 pandemic, and—most critically—the external debt default, which sharply reduced immediate foreign exchange outflows.

However, emerging global headwinds—particularly the escalating Iran–US conflict—are beginning to pose new risks to the external sector. The conflict has driven up global energy prices and heightened uncertainty in financial markets, which could increase Sri Lanka’s import bill, especially for fuel, while also dampening external demand and investor sentiment. At the same time, short-term pressures could intensify due to higher capital imports linked to reconstruction and infrastructure development, the absence of effective incentives for investment and export-oriented sectors, taxes on digital remittance channels, and persistently negligible new FDI inflows. Collectively, these factors create meaningful vulnerabilities for the BOP outlook in 2026.

Even so, the BOP is expected to remain modestly positive in 2026, though with rising downside risks. Continued gains in remittances and tourism earnings should provide some support, but both are exposed to spillover effects from the conflict—particularly if economic conditions in the Middle East weaken, affecting remittance flows, or if global travel demand softens. In addition, reduced external debt servicing obligations during the year should ease near-term pressure on reserves, while targeted import management and a gradual export recovery could help maintain external stability.

Accordingly, although reconstruction-related imports and demand for capital goods may widen the trade deficit—further exacerbated by higher global oil prices—sustaining a BOP surplus in 2026 will hinge on preserving resilient remittance inflows, expanding service exports, attracting stable long-term foreign investment, and navigating the external shocks arising from ongoing geopolitical tensions.

STOCK MARKET

Prediction for 2026:

The ASPI is likely to resume its upward trajectory by

mid-2026, assuming there will not be some political turmoil or oil shocks

Outlook for 2026

As anticipated at the outset of the year, the Colombo Stock Exchange sustained a steady upward trajectory through much of 2025, supported by easing interest rates, improving liquidity conditions, and a recovery in corporate earnings. However, this positive momentum is now showing signs of moderation.

The economic fallout from Cyclone Ditwah, combined with escalating geopolitical tensions arising from the US–Iran conflict, has introduced a new layer of uncertainty to the outlook. In particular, heightened volatility in global crude oil prices driven by fears of supply disruptions in the Middle East—poses a direct risk to Sri Lanka’s macroeconomic stability. As a net fuel importer, rising oil prices are expected to widen the trade deficit, exert pressure on the currency, and reintroduce inflationary concerns, all of which could weigh on investor sentiment.

Against this backdrop, the market is increasingly vulnerable to a near-term correction. Elevated global risk aversion, coupled with concerns over higher energy costs, fiscal strain from reconstruction spending, and delays in economic normalization, may prompt investors to reassess earnings expectations across key sectors. The ASPI, therefore, faces the possibility of a late-cycle pullback as these risks are priced in.

That said, the medium-term investment case for Sri Lankan equities remains intact.

Valuations continue to appear attractive particularly in US dollar terms while the underlying fundamentals of listed corporates show resilience. Although the ongoing conflict may trigger intermittent volatility, especially in energy-sensitive, transport, manufacturing, and import-dependent sectors, the direct impact of the cyclone on listed equities is expected to be largely transitory.

The broader market outlook continues to be supported by several structural factors:

- Strengthening corporate balance sheets alongside a gradual easing in financing costs

- Continued recovery in external inflows from tourism, worker remittances, ICT, and logistics subject to global stability

- Progress in structural reforms, including fiscal consolidation efforts and potential state-owned enterprise restructuring

In sum, while near-term downside risks have risen due to the combined effects of domestic disruptions and external shocks particularly those linked to oil price fluctuations amid the US–Iran conflict the Colombo Stock Exchange still offers compelling medium-term upside potential. Sustaining this trajectory, however, will depend critically on maintaining macroeconomic stability and ensuring that global energy and geopolitical pressures do not intensify further.

COMMODITY PRICES

TEA

RUBBER

CRUDE OIL

Commodity price movements are likely to be mixed in early 2026.

- Crude oil prices have surged past USD 100 per barrel in March 2026 and are expected to remain highly volatile amid the escalating US–Iran conflict and risks surrounding potential disruptions to the Strait of Hormuz.

- Any prolonged or partial closure of this కీల chokepoint could significantly constrain global supply, further elevating prices and placing substantial pressure on Sri Lanka’s import bill.

- For a fuel-import dependent economy, higher oil prices will translate into increased transportation, electricity, and industrial input costs, even as domestic pricing reforms help limit direct subsidy losses.

- Commodity price trends are therefore expected to exert a more pronounced drag on trade and inflation in early 2026, with elevated oil prices widening the trade deficit and intensifying cost-push inflation.

- These pressures may be partly cushioned by remittance inflows and tourism earnings, although both remain vulnerable to spillover effects from the conflict, particularly in the Middle East.

- Tea output weakened toward year-end due to heavy rains and cyclone-related disruptions, while lower production and a weaker rupee pushed auction prices higher in local currency terms.

- Although stronger global tea prices have supported export revenues, logistical constraints and selective quality issues may limit further upside.

- Tea exports face additional downside risks due to the US–Iran conflict, as Iran is one of the largest buyers of Ceylon tea, and disruptions to trade flows, payment channels, and economic conditions could weaken demand.

- Shipping disruptions through the Strait of Hormuz may further hinder exports to the Middle East, a key destination for Sri Lanka’s tea shipments.

- Tea prices are expected to remain volatile amid uneven weather patterns and lingering crop losses from Cyclone Ditwah, with short-term supply tightness supporting prices but potentially reducing export volumes.

- Overall, commodity price movements—now heavily influenced by oil market volatility and geopolitical risks—are expected to have a neutral-to-slightly negative impact on Sri Lanka’s external performance, with risks tilted to the downside if supply disruptions intensify.

TOURIST ARRIVALS

UNEMPLOYMENT

CAR REGSITRATIONS