FINANCIAL CHRONICLE – The Sri Lankan rupee is currently experiencing significant pressure, primarily due to the central bank’s decisions that have undermined market confidence. This includes excess liquidity stemming from currency swaps and erratic interventions in the market. Despite these challenges, certain sectors remain insulated from macroeconomic influences.

Since late 2024, the central bank has systematically undermined the rupee by employing aggressive monetary policies and manipulating exchange rates, often disregarding monetary stability and social harmony. The parliamentary Committee on Public Finance has issued multiple warnings regarding the risks associated with buy-sell swaps, as well as the potential dangers of acquiring dollars at depreciated rates, which have arisen from an excess of balance of payments surplus resulting from deflationary bond coupon effects and natural growth in reserve money.

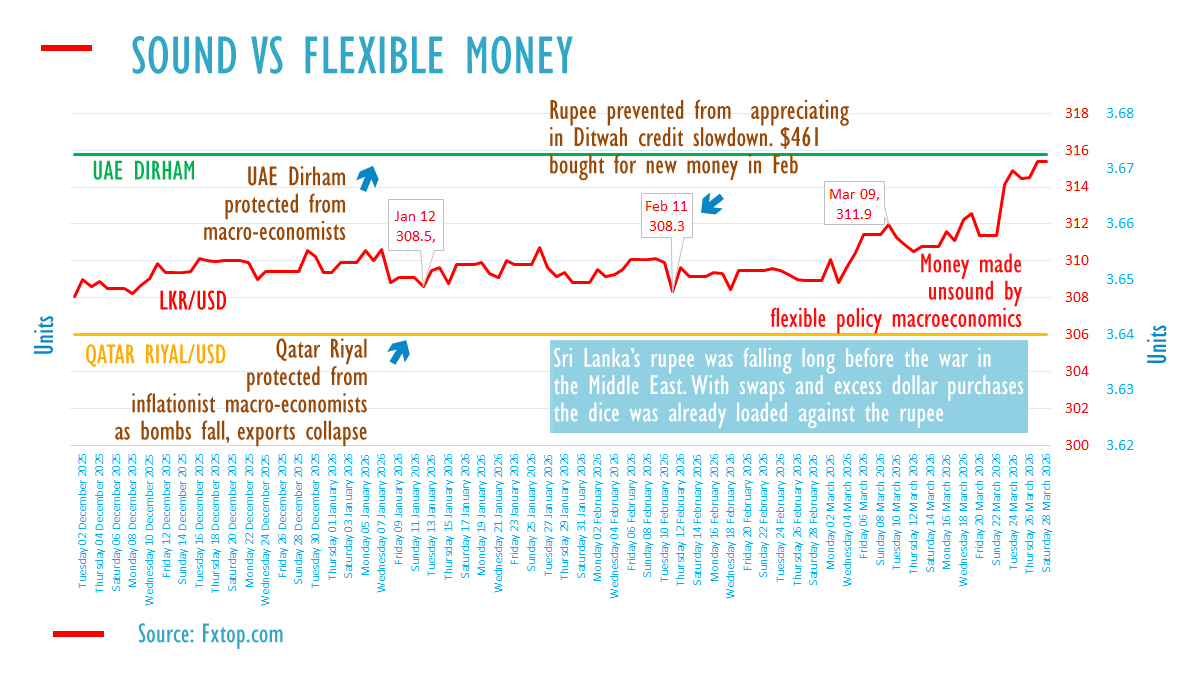

In contrast to the proactive measures taken by the central bank leadership in 2004, following the tsunami when they allowed the rupee to appreciate, a harsh display of inflationist policies led to the extraction of $461 million from the market in February 2025. Initial warnings regarding the rupee’s stability last year were primarily due to the central bank’s excessive dollar purchases, which did not initially trigger panic or loss of confidence among investors. However, the current scenario is markedly different, characterized by a significant loss of faith in the currency and an overwhelming excess of liquidity.

The instability appears rooted in the flawed operational framework of the independent monetary authority. A prevalent misconception among nations that frequently seek assistance from the IMF is that currency values are determined by market forces. Sound economic principles, including the laws of supply and demand, rely on stable monetary conditions rather than inflationary pressures or competitive exchange rates favored by certain macroeconomic theorists.

In reality, the value of currency should not be determined by market forces; rather, it should be anchored to provide stability in a market economy, ensuring social cohesion and democratic governance. Under a clean floating exchange rate regime, the central bank manages the currency’s value through monetary policy and interest rates, albeit with some delay. In contrast, a fixed exchange rate eliminates monetary policy, tying the currency to another with low inflation and preventing macroeconomic mismanagement.

The flexible exchange rate system has been used against the populace and elected governments for over a year, contributing to the rupee’s depreciation from 297 to 310 in 2025. The recent conflict in the Middle East has further exacerbated economic instability, with macroeconomic policies amplifying the impacts by increasing energy costs and creating a rift between the government and its constituents.

Following the stabilization crises of 2017 and 2019, the subsequent government was keen to enhance potential output through IMF-style policies, thereby aligning with the central bank’s actions. However, during Mangala Samaraweera’s tenure as Finance Minister, a more cautious approach was adopted involving tax increases to manage deficits, though he faced constraints from macroeconomic influences within the central bank.

In 2018, the central bank’s aggressive monetary policies, including printing money and implementing swaps, led to significant economic challenges, prompting calls for a return to a more stable monetary regime. Despite the central bank’s de facto independence, the government struggled to control its monetary policy effectively.

As the economy faced rising challenges, including foreign investors pulling out due to the flexible exchange rate, the government resorted to international borrowing, leading to further complications. The macroeconomic strategy included a controversial approach that prioritized potential output targeting, reminiscent of failed full employment policies from the past.

The flexible exchange rate system, characterized by arbitrary interventions, has proven detrimental to the rule of law and democratic governance. Such systems can lead to unpredictable government actions that undermine economic stability and public trust.

Recent developments, including the introduction of a single policy rate and continued reliance on a flexible exchange rate, have raised concerns regarding the sustainability of monetary stability and the ability to service external debts. The central bank’s approach has been widely criticized as an escape route from accountability, particularly in light of rising inflation and external economic shocks.

Looking ahead, the central bank must consider unwinding its swap agreements and selling dollars to the Treasury to restore stability to the rupee. By reducing excess liquidity, the central bank can mitigate the need for further dollar sales in the import market. Additionally, the government should pursue strategies to build its reserves independently of central bank influences, ensuring a more resilient economic framework.

The situation in Sri Lanka serves as a stark reminder of the importance of sound monetary policies and the risks posed by macroeconomic mismanagement. In light of the significant challenges ahead, a reevaluation of the current policies is crucial to restore confidence and stability in the economy.